Post COVID-19 World: The Bullish Case for (early stage) VCs & Founders [Part 2]

Exits: IPOs and M&A Landscape

Initial Public Offerings – IPOs

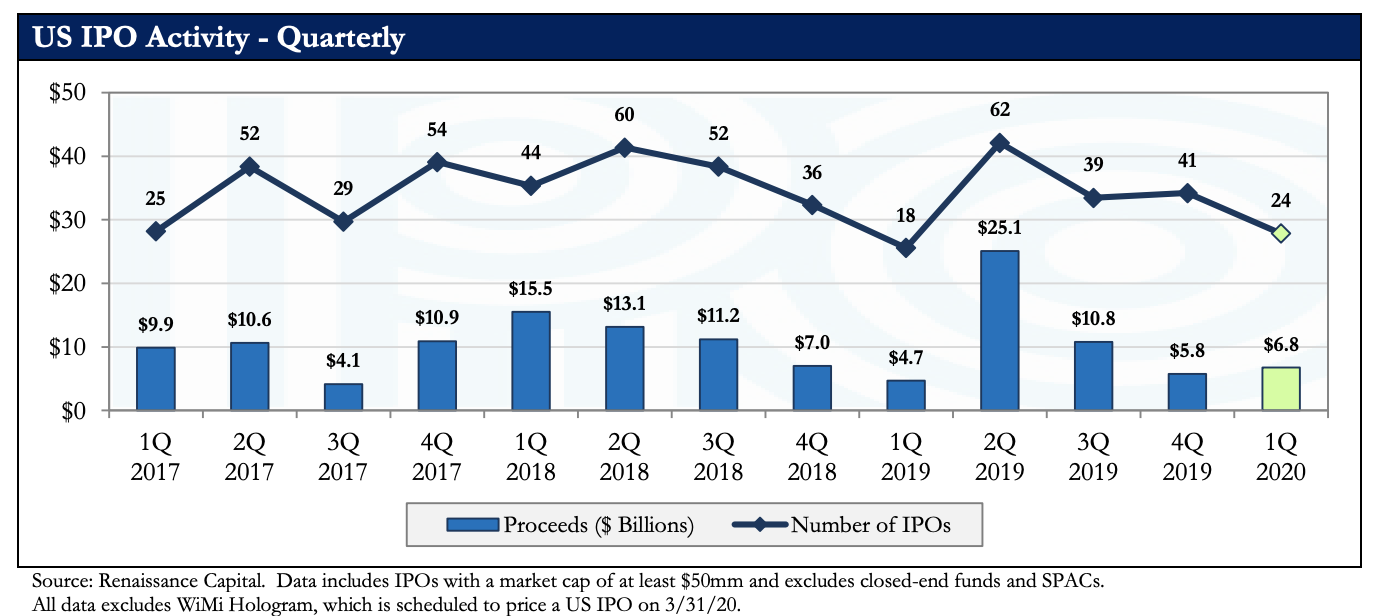

According to the Renaissance Capital research note of March 27, 2020, “The 2020 IPO market began with optimism and ended with the worst crash since the global financial crisis. 24 IPOs raised $6.8 billion, with as many as 20 companies forced to shelve offerings when the IPO window slammed shut in early March, as the focus of investors and policy-makers shifted to a post-coronavirus paradigm….Healthcare was both the most active and best-performing sector, accounting for half of all IPOs and averaging a 24% return, with drug development platform Schrödinger and health clinic One Medical performing well.”

Overall, Q1-2020 was a strong quarter, with half of the deals being Healthcare related, and biotechs driving activity and outperformance. It was significantly higher than Q1-2019, but lower than expected due to the Coronavius affecting the second half of March. As a result of the window shutdown, as many as 20 IPOs are delayed and await re-opening.

We can certainly expect the IPO window to remain shut until after the summer, which will exacerbate the issues for late stage private companies burning a lot of cash. They may need to seek another late stage private round, with significant downward valuation pressure. The window will eventually re-open, as it always does, with high quality companies leading the way, while others may seek an M&A alternative.

We can expect healthcare companies to continue leading the way in the IPO segment over the next few quarters, as the world starts to massively invest in healthcare solutions and infrastructure (see more below on the case for AI and Healthcare). Additionally, we can expect Enterprise Software to do well as corporations around the world seek to increase productivity by empowering their employees, irrespective of their locations (office or home), or reduce their dependence on employees all together. As Aaron Levie, the CEO of Box, said in a tweet on March 28, 2020:

As is always the case after a major market crisis, the bar will be raised and further scrutiny will be applied to companies going public. Investors will likely take a much closer look at supply chain resilience/risks and the capabilities of these businesses to cope with future pandemic-like disruption, remote working capacity, etc.

If the bar gets too high, it will further delay high growth companies from going public, and if Wall Street short-term investor views do not fit the companies focus on customer lifetime value (LTV) and acquisition costs (CAC), then it is likely that innovative, VC-backed, high-growth companies may seek alternative listing on Silicon Valley’s Long Term Stock Exchange.

Mergers and Acquisitions – M&As

Like the IPO market, we can expect M&A to pause as buyers start to look inward and evaluate the immediate and longer term implications of COVID-19 on their business. Deals in progress may also be delayed, as transaction value gets renegotiated, and synergies get re-evaluated.

Speaking with a former head of Global M&A deal at Google during the 2007-2008 Global Financial Crisis, he said “the company, despite being one most active acquirers at the time, did a complete halt of its M&A activity for a period of 6-9 months, but that was immediately followed by one of the most active M&A periods in the history of the company, with more than a deal per week for a sustained period of 12 months”.

We can probably expect a similar “wait and see” period from most corporations, but the smart one should start acquiring smaller tech companies and their teams that will be seeking safe-harbor. Beside the digital leaders of today (most of which were born-digital), most corporations from the prior industrial era have been failing to “digitalize” fast enough, or at all. These companies will be facing significant pressure from their boards and shareholders to “aggressively” invest in their digital transformation, and M&A will become a very valuable tool for them to acquire valuable technology and talent they have not been able to develop and nurture in-house.

With $1.5T on the balance sheet of US Corporations at the end of 2019, I fully expect an acceleration of Tech M&A deals, especially in the $50-500M range.

Additionally, buy-out funds were sitting on $760B of dry powder at the end of 2019 (a historic high) and debt financing rates are likely to go down as well.

Historically PE firms have shied-away from what they consider the highly priced technology (and mostly venture-backed) sector. But as technology (and especially AI/ML) companies start to be perceived as potential proprietary margin enablers to transform their portfolio companies, PE firms may reconsider how they measure the ROI of such acquisition. What if such an acquisition could lift each of their portfolio company’s profitability by 10-40% – in addition to their financial engineering and management strategies? This would be a total game changer for the fund that could master this strategy.

However, buy-out firms will first need to manage the fact that many of their portfolio companies are burdened with debt, a model that significantly reduces a company’s operational margin of error. Many PE-backed companies could soon default on their debt covenants, sending most PE firms scrambling and slowing down their ability to engage in new investments or acquisitions for months to come.

According to research firm The 415 Group, 2019 saw more tech M&A deals than 2018 (3,640 vs. 3,617), but the total transaction volume fell by 20% to $461B as historical key acquirers such Oracle, Microsoft, IBM and SAP did not ink a single deals over $1Bn. These acquirers could come back with a vengeance in 2020, or new tech firms born in the past two decades could continue to take over as leading acquirers and displace older, more-established buyers.

The US should continue to attract the majority of M&A deals, as per the chart below, and it bodes well for the Venture Capitalists that are backing these companies.

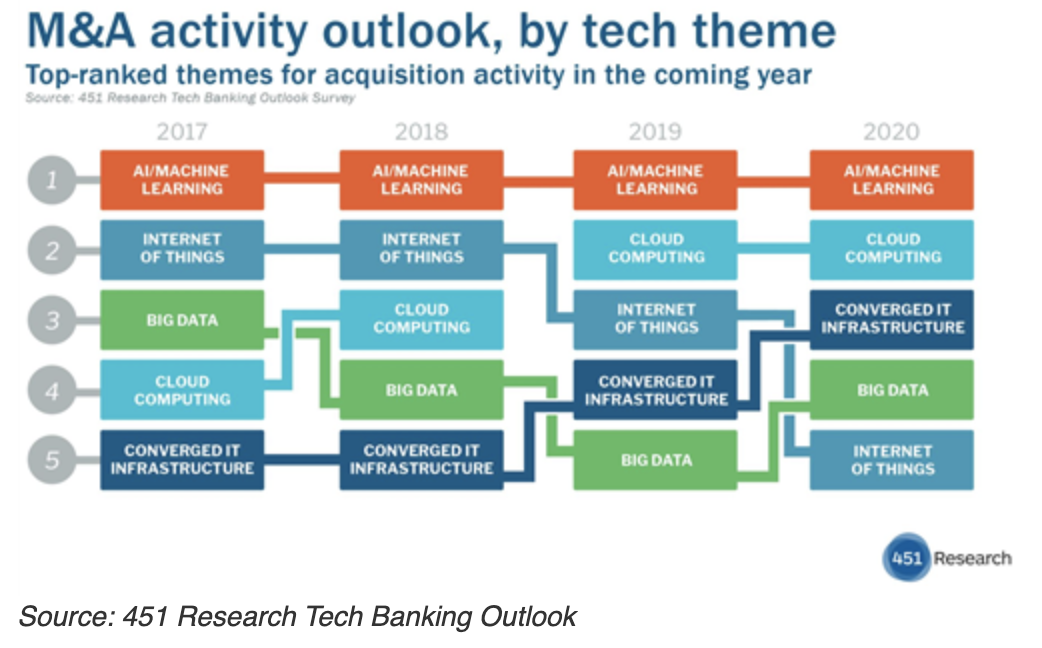

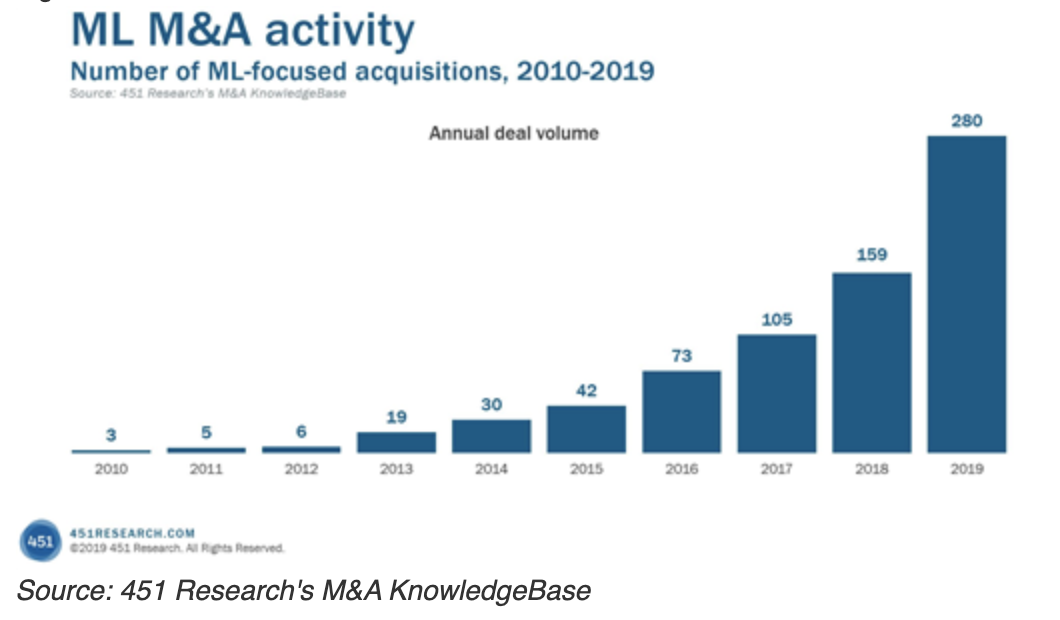

Not all M&A themes are created equal, and when it come to AI and ML technology, which is BootstrapLabs’ core investment focus, that theme has been ranking #1 in terms of priority for acquirers, and the volume has been growing exponentially (see charts below).