Venture: Seed is the New Series A

In a world where access is king and real “value-add” to startup founders creates true differentiation, some Series A (and even Seed) VC firms are in for a rude awakening.

The Shift

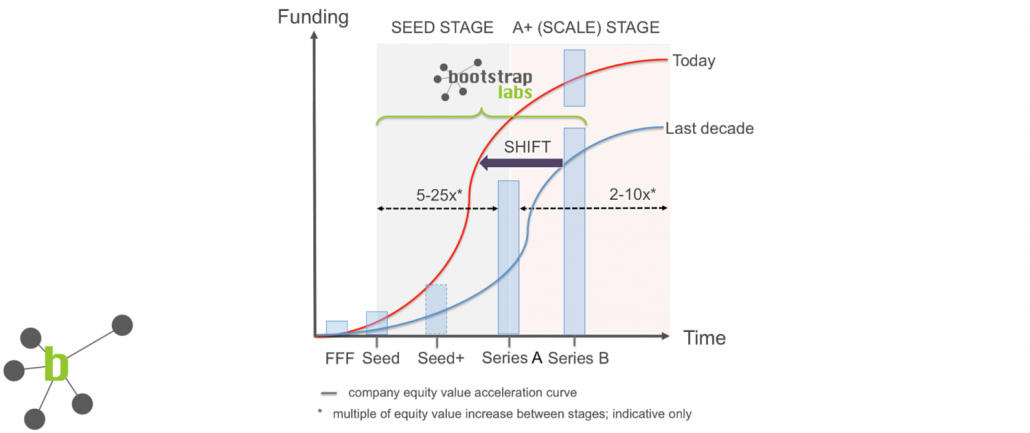

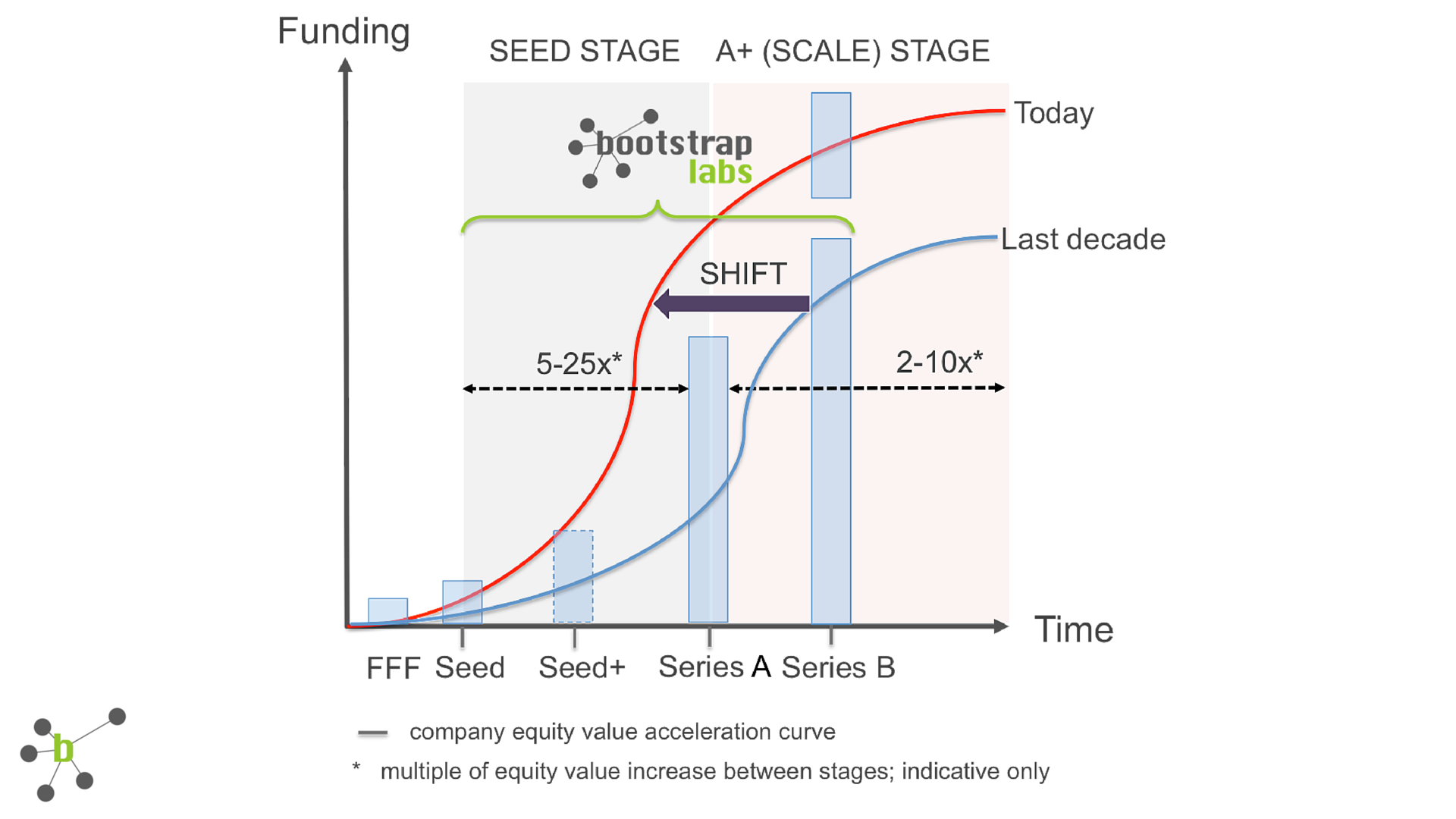

Seed is the New Series A captures much of what is going on in the startup and VC world these days. The cost of building technology startups has plummeted by a factor of 5 – 10x in the last decade, resulting in founders often needing far less capital and time to achieve similar results.

A startup typically remains in its seed stage until it has tested and validated a scalable product market fit. Then they shoot for a Series A round of funding from a top VC firm that could ideally take them all the way to an IPO or an exit.

In many respects, the level of maturity and risk associated with these Series A companies would be equivalent to the Series B and C rounds from a decade ago. Yet, VCs are still calling them Series A rounds since it is usually the first investment they would make in a startup.

The chart below is an attempt at visualizing the shift that took place in the equity value creation acceleration curve in relation to the various financing rounds of a successful, but not out of this world (e.g. Uber, Slack, etc.) startup.

Investment, Stages and Equity Value Creation

The reduction in Series A risk profile certainly explains some of the increased Series A round size and associated valuation. You would think that the much talked about Series A crunch would have kept the valuations in check, but truth be told, not every company can clear the Series A bar, and when they do, every investor wants in.

If Series A VCs were previously rewarded for taking risk, having the ability to “pick” potential winners early, and help the founders craft and shape their companies, that know-how appears to have now migrated toward the seed stage investors.

Naval Ravikant recently addressed VCs, saying: “you can lie to your LPs but don’t lie to yourself, you are doing series B and C rounds these days.”

Another brilliant quote came from Sumon Sadhu (wrongly attributed to Dave Morin in the article) who said during the NVCA annual meeting that: “today, when VCs get involved in a startup, 900 of the 1000 first critical decision have been made.”

The proverbial VC quote: “we are value-add guys”

So how much value are VCs really providing entrepreneurs these days?

Fred Wilson recently wrote on his blog about What VC can learn from Private Equity, “there is a lot of talk about value add from VCs, but often that is just for show during the process of winning the deal. The number of VCs who actually add a lot of value to their investments is much smaller than you would think.”

In another interesting twist, Silicon Valley startups can and must go global faster than ever before if they want to avoid being copied by professional cloning factories such as Rocket Internet. Which brings up another troubling fact: the vast majority of VC firms, including some of the most well known in Silicon Valley, have little to no experience helping their startups scale globally.

Some critics have even gone as far as accusing traditional VCs of becoming money managers and that the only benefit one would find in raising money from a VC is the size of the check they can cut.

In today’s world, a good entrepreneur has the ability to pick his investors. If the ones providing the most help are their seed investors, then it is likely that these same seed investors will be invited to participate or even lead their Series A round.

Our latest blog post on The Rise of Angel(List) definitely shows how Syndicates and SPVs can be leveraged by angels and earlier stage funds in order to participate and even lead in later stage rounds.

BootstrapLabs follows these trends closely and after years of providing high-touch hands-on value-add work with the founders of each of our portfolio companies, we are on the verge of launching a very tangible, scalable, and disruptive way to deliver value to all our founders. Stay tuned for more …

and how it is rapidly changing the game of angel investing")